We offer free report customization services, whether you purchase a stand-alone chapter or a country-level report. Additionally, we provide affordable discounts for startups and universities.

Market Overview

Effective insulation is a crucial component in maintaining ideal internal conditions within buildings, vehicles, and enclosed environments. Proper insulation regulates interior temperatures, excludes external elements, and provides acoustic dampening. This offers several important benefits:

In buildings, insulation is applied to walls, roofs, floors, and foundations to limit heat transfer between the interior and exterior. Insulating a structure can reduce heating and cooling costs by over 40%, providing significant energy savings over time. By preventing conduction, convection and air leakage, insulation enables a consistent, comfortable indoor climate while minimizing energy demand. It also mitigates moisture accumulation and condensation issues.

Transportation insulation is vital for passenger comfort and temperature control. Engine compartments, cabins, and sensitive equipment are shielded from temperature swings, road noise and aerodynamic buffeting. Insulation reduces vibrations and sound transmission. It extends component life by protecting against corrosion. Weight savings can also improve vehicle efficiency and range. This study analyzes advanced insulation materials with exceptionally high R-values per inch of thickness (R-values over 20/inch). The major material types explored include:

Vacuum Insulated Panels (VIPs) – These consist of a core material contained within an air-tight envelope with vacuumized interior. The evacuated environment virtually eliminates conductive and convective heat transfer, enabling remarkable R-values of over 40 per inch. VIPs deliver superior insulation performance in a slim form factor, ideal for space-constrained applications. However, long-term vacuum retention and durability issues must be addressed.

Aerogels – Extremely porous synthetic materials with nanoscale pore structures that suppress solid conduction and gaseous convection. Silica-based aerogel blankets and particles can achieve R-values above 20 per inch. Key benefits include lightweight, hydrophobicity, acoustic damping and flexibility. Drawbacks currently include high costs and brittleness.

Polyimide Foams – Low-density cellular plastics composed of polyimide polymer matrices. The closed-cell structure traps gas (air or inert gas), impeding conductive and convective heat flow. R-values range from R-20 to R-30/inch. Polyimide foams offer high-temperature stability and dielectric strength. However, the materials are relatively expensive.

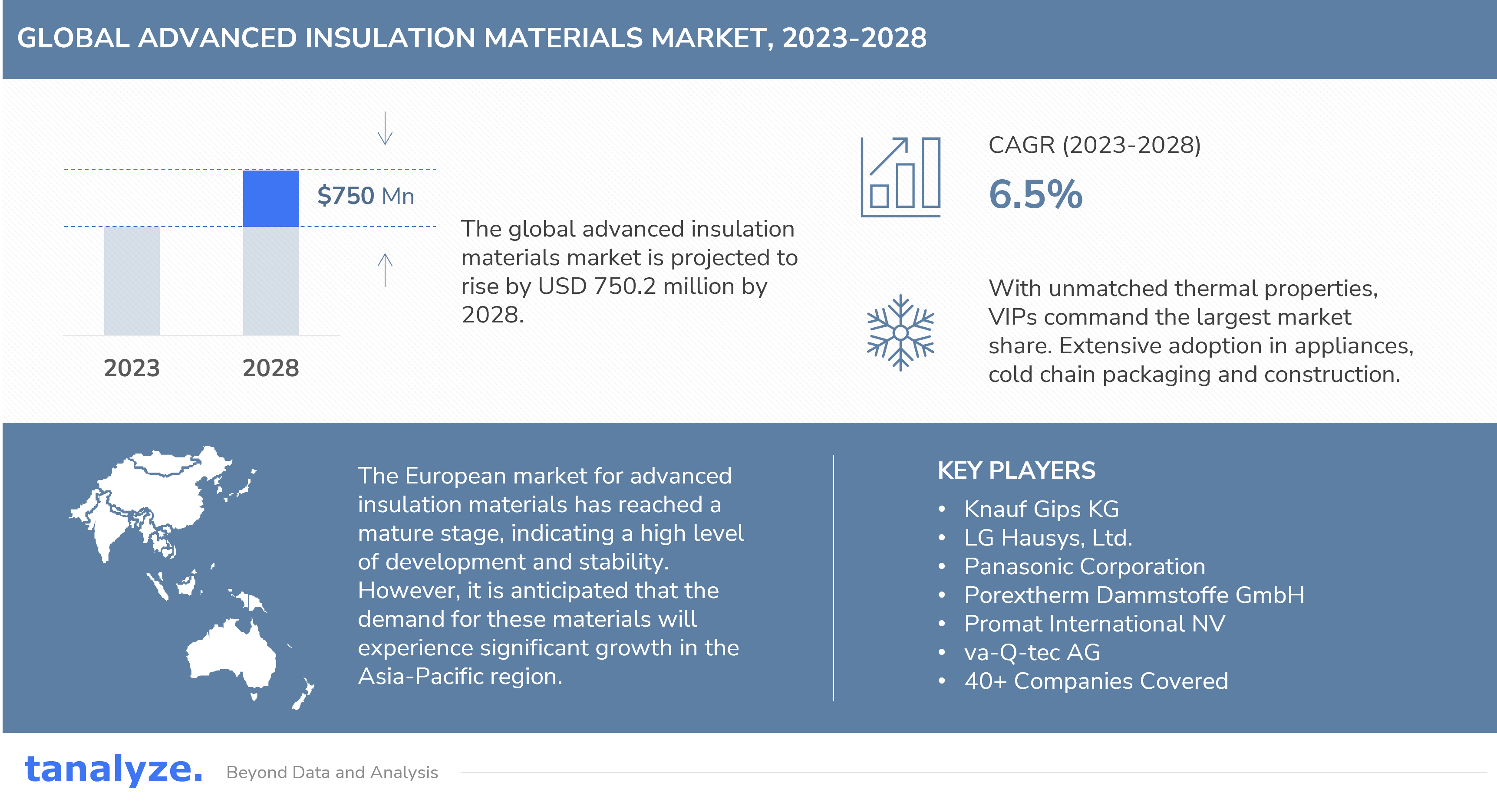

According to the most recent market study, the global advanced insulation materials market exhibited a value of USD 1,903 million in 2022. Over the forecast period from 2023 to 2028, the market is projected to witness significant growth, reaching a value of USD 2,777 million. This represents a compound annual growth rate (CAGR) of 6.5%.

This report offers a comprehensive statistical analysis tailored specifically to the advanced insulation materials sector, arming stakeholders with the quantitative insights needed to evaluate the landscape and capitalize on growth opportunities.

Research Coverage

The report provides a detailed analysis of the following segments within the advanced insulation materials market: By product – aerogels (carbon aerogels, metal aerogels, and silica aerogels), polyimide foams (thermoplastic polyimide foams, and thermosetting polyimide foams), vacuum insulated panels (fiberglass VIPs, and fumed silica VIPs), and others. By end user – automotive and aerospace, building and construction, marine and defense, oil and gas, refrigeration, transportation and warehousing, and others. By region – Americas, Europe, Asia-Pacific, and Rest of World.

The global advanced insulation materials market can be divided into four primary categories based on product type. Vacuum insulated panels, or VIPs, currently contribute the most to the market. VIPs provide highly effective insulation with very thin designs by having a gas-evacuated core between two thin, highly conductive panels.

This product segment dominated the advanced insulations market owing to the remarkably high R-values and space efficiency offered by VIPs. Their unsurpassed thermal performance has led to extensive adoption in appliances, cold chain packaging, and building construction. VIPs currently account for the largest revenue share in the market.

Based upon end user, the global advanced insulation materials market is categorized into automotive and aerospace, building and construction, marine and defense, oil and gas, refrigeration, transportation and warehousing, and others. The extensive usage of advanced insulations in refrigeration stems from the need for extremely efficient thermal barrier materials to maintain cryogenic temperatures during food and vaccine cold chain distribution. Vacuum insulated panels enable optimizing the insulation-to-space ratio in compact refrigerated packaging and cold storage facilities.

Superior moisture resistance also makes advanced insulations well-suited for inhibiting ice formation and condensation issues. Key applications include insulating refrigerated trucks, cold storage warehouses, blood banks, laboratory equipment, and liquefied natural gas tankers among others. Demand is surging due to rising global consumption of perishable foods, increasing pharmaceutical cold chain logistics, and expansion of liquefied natural gas infrastructure. In addition, sustainability initiatives targeting greenhouse gas emission reductions are further propelling adoption.

The growing adoption of electric vehicles is poised to drive demand for advanced insulation materials within the automotive industry. EVs require specialized thermal management solutions to maintain optimal temperature ranges for batteries and power electronics. Advanced materials like aerogels, polyimide foams and vacuum insulated panels enable thinner, lighter insulation with higher efficiency. As EVs gain broader consumer acceptance and battery packs increase in size, insulation will take on greater importance in vehicle design and performance.

Additionally, the global trend toward renovating and retrofitting existing residential and commercial buildings to improve energy efficiency will spur the use of advanced insulation materials in the construction sector. Building owners are increasingly seeking to upgrade exterior walls, roofs and foundations with high-performance insulations that provide superior R-values within slimmer profiles. This allows improving thermal performance while minimizing alteration of existing structures.

Regulatory policies are further supporting adoption of advanced insulations. Stringent building codes and product standards aimed at reducing energy consumption, as well as sustainability initiatives targeting greenhouse gas emissions, are creating incentives for developers and contractors to utilize cutting-edge insulation materials. Related government incentives and rebates also help offset the higher costs of these materials.

Geographically, the global advanced insulation materials market is segmented into Americas, Europe, Asia-Pacific, and Rest of World. The European market for advanced insulation materials has reached a mature stage, indicating a high level of development and stability. However, it is anticipated that the demand for these materials will experience significant growth in the Asia-Pacific region. This is primarily due to the region’s increasing emphasis on alternate fuel technologies for both private and public transportation.

In recent years, there has been a notable shift towards adopting alternative fuels in the Asia-Pacific region, driven by concerns over environmental sustainability and the need to reduce carbon emissions. As a result, there is a growing demand for advanced insulation materials that can enhance the efficiency and performance of these alternative fuel technologies.

Furthermore, there is a strong focus on improving fuel efficiency in the automotive industry worldwide. Original Equipment Manufacturers (OEMs) are actively working towards reducing the weight of vehicles as a means to achieve this goal. By incorporating advanced insulation materials into the design and manufacturing processes, OEMs can effectively reduce the overall weight of vehicles without compromising on safety or performance.

Looking for Customization?

Customize your report by selecting specific countries or regions and save 30%

The global market for advanced insulation materials is characterized by intense competition among various industry players. Leading companies in this market include 3M Company, Active Aerogels Lda. (Grupo BEL), Aerogel Technologies LLC, American Aerogel Corporation, Armacell LLC, ASAHI FIBER GLASS Co. Ltd., Aspen Aerogels Inc., BASF SE, Boyd Corporation, Cabot Corporation, Chuzhou Yinxing New Materials Technology Co. Ltd., Compagnie de Saint-Gobain S.A. (ISOVER), CSafe Global LLC, Dow Inc., Enersens SAS, Etex S.A. (Promat International NV), Evonik Industries AG, Fujian SuperTech Advanced Material Co. Ltd., Guangdong Alison High-tech Co. Ltd., Hitachi Ltd., Isoleika S. Coop., Jiangsu Sanyou Dior Energy-Saving New Materials Co. Ltd., JIOS Aerogel Pte Ltd., Kingspan Group plc, Knauf Gips KG, Kurabo Industries Ltd., KyungDong One Co. Ltd., LG Hausys Ltd., Morgan Advanced Materials plc (Porextherm Dammstoffe GmbH), Nano Tech Co. Ltd., OCI Company Ltd., Panasonic Corporation, PBM Insulations Pvt. Ltd., Protective Polymers Ltd., Sealed Air Corporation (Kevothermal LLC), Sichuan Micolon Vacuum New Material Co. Ltd., Siltherm Group Holdings Limited, Svenska Aerogel Holding AB, TAASI Corporation, Trelleborg AB, TURNA d.o.o., Turvac inovativne izolacije d.o.o., Vaku-Isotherm GmbH, and va-Q-tec AG.

These companies play a crucial role in driving the growth of the advanced insulation materials market through their active contributions in terms of innovation and product development. They continuously strive to introduce new and improved insulation materials that offer enhanced thermal efficiency, durability, and environmental sustainability. By investing in research and development, these companies aim to meet the evolving needs of various industries, such as construction, automotive, aerospace, and energy.

Advanced Insulation Materials Industry Developments

▸ June 12, 2023 – The Bundeskartellamt has approved plans for EQT Fund Management S.à.r.l. to acquire shares and assume full control of Germany’s va-Q-tec AG, a provider of thermal insulation and cold chain logistics solutions. EQT, a Luxembourg-based private equity firm, already controls Sweden’s Envirotainer AB, which develops, manufactures, and leases temperature-controlled containers used mainly for biopharmaceutical air transport. This acquisition will strengthen EQT’s position in the global cold chain logistics sphere. ▸ Feb. 17, 2022 – Aspen Aerogels to receive $150M investment from Koch Strategic Platforms. The funding will support Aspen’s growth in aerogel thermal barrier solutions. Koch acquired convertible notes and Aspen common stock. Aspen is a leader in sustainable aerogel-based technologies for thermal management applications.

Key Questions Answered

What is the projected global market size of advanced insulation materials by 2028? Which product segment possesses the largest market share? Which end user segment demonstrates the most significant dominance? In terms of market dominance, which region segment prevails in the advanced insulation materials market? Who are the key players with the largest market share in the advanced insulation materials market? What is the estimated global market size for the advanced insulation materials market in 2023? What are the main factors driving the growth of the advanced insulation materials market? What is the expected incremental growth of the advanced insulation materials market during the forecast period?

Report Coverage

Details

Market Size

USD 1903.3 million in 2022

CAGR (2023-2028)

6.5%

Base Year

2022

Forecast Period

2023-2028

Pages

95

Segments

Product, End User, Region

Regions Covered

Europe, Americas, Asia-Pacific, Rest of World

Key Players

3M Company, Active Aerogels Lda. (Grupo BEL), Aerogel Technologies LLC, American Aerogel Corporation, Armacell LLC, ASAHI FIBER GLASS Co. Ltd., Aspen Aerogels Inc., BASF SE, Boyd Corporation, Cabot Corporation, Chuzhou Yinxing New Materials Technology Co. Ltd., Compagnie de Saint-Gobain S.A. (ISOVER), CSafe Global LLC, Dow Inc., Enersens SAS, Etex S.A. (Promat International NV), Fujian SuperTech Advanced Material Co. Ltd., Guangdong Alison High-tech Co. Ltd., Hitachi Ltd., Isoleika S. Coop., Jiangsu Sanyou Dior Energy-Saving New Materials Co. Ltd., JIOS Aerogel Pte Ltd., Kingspan Group plc, Knauf Gips KG, Kurabo Industries Ltd., KyungDong One Co. Ltd., LG Hausys Ltd., Morgan Advanced Materials plc (Porextherm Dammstoffe GmbH), Nano Tech Co. Ltd., OCI Company Ltd., Panasonic Corporation, PBM Insulations Pvt. Ltd., Protective Polymers Ltd., Sealed Air Corporation (Kevothermal LLC), Sichuan Micolon Vacuum New Material Co. Ltd., Siltherm Japan Limited, Svenska Aerogel Holding AB, TAASI Corporation, Trelleborg AB, TURNA d.o.o., Turvac inovativne izolacije d.o.o., Vaku-Isotherm GmbH, va-Q-tec AG

Table of Contents

1. Scope and Methodology 1.1 Introduction 1.2 Report Scope 1.3 Research Methodology 2. Executive Summary 3. Market Overview 4. Global Advanced Insulation Materials Market – Product Analysis 4.1 Aerogels 4.2 Polyimide foams 4.3 Vacuum insulated panels (VIPs) 4.4 Others 5. Global Advanced Insulation Materials Market – End User Analysis 5.1 Automotive and aerospace 5.2 Building and construction 5.3 Marine and defense 5.4 Oil and gas 5.5 Refrigeration 5.6 Transportation and warehousing 5.7 Others 6. Global Advanced Insulation Materials Market – Region Analysis 6.1 Americas 6.2 Europe 6.3 Asia-Pacific 6.4 Rest of World 7. Patents Analysis 8. Competitive Landscape 8.1 Competitive Scenario 8.2 Market Positioning/Share Analysis 8.3 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements 9. Company Profiles 9.1 3M Company 9.2 Active Aerogels, Lda. (Grupo BEL) 9.3 Aerogel Technologies, LLC 9.4 American Aerogel Corporation 9.5 Armacell LLC 9.6 ASAHI FIBER GLASS Co., Ltd. 9.7 Aspen Aerogels, Inc. 9.8 BASF SE 9.9 Boyd Corporation 9.10 Cabot Corporation 9.11 Chuzhou Yinxing New Materials Technology Co., Ltd. 9.12 Compagnie de Saint-Gobain S.A. (ISOVER) 9.13 CSafe Global, LLC 9.14 Dow Inc. 9.15 Enersens SAS 9.16 Etex S.A. (Promat International NV) 9.17 Evonik Industries AG 9.18 Fujian SuperTech Advanced Material Co., Ltd. 9.19 Guangdong Alison High-tech Co., Ltd. 9.20 Hitachi, Ltd. 9.21 Isoleika S. Coop. 9.22 Jiangsu Sanyou Dior Energy-Saving New Materials Co., Ltd. 9.23 JIOS Aerogel Pte Ltd. 9.24 Kingspan Group plc 9.25 Knauf Gips KG 9.26 Kurabo Industries Ltd. 9.27 KyungDong One Co., Ltd. 9.28 LG Hausys, Ltd. 9.29 Morgan Advanced Materials plc (Porextherm Dammstoffe GmbH) 9.30 Nano Tech Co., Ltd. 9.31 OCI Company Ltd. 9.32 Panasonic Corporation 9.33 PBM Insulations Pvt. Ltd. 9.34 Protective Polymers Ltd. 9.35 Sealed Air Corporation (Kevothermal, LLC) 9.36 Sichuan Micolon Vacuum New Material Co., Ltd. 9.37 Siltherm Group Holdings Limited 9.38 Svenska Aerogel Holding AB 9.39 TAASI Corporation 9.40 Trelleborg AB 9.41 TURNA d.o.o. APPENDIX DISCLAIMER

Companies Mentioned

A selection of companies mentioned in this report includes: 3M Company Active Aerogels, Lda. (Grupo BEL) Aerogel Technologies, LLC American Aerogel Corporation Armacell LLC ASAHI FIBER GLASS Co., Ltd. Aspen Aerogels, Inc. BASF SE Boyd Corporation Cabot Corporation Chuzhou Yinxing New Materials Technology Co., Ltd. Compagnie de Saint-Gobain S.A. (ISOVER) CSafe Global, LLC Dow Inc. Enersens SAS Etex S.A. (Promat International NV) Evonik Industries AG Fujian SuperTech Advanced Material Co., Ltd. Guangdong Alison High-tech Co., Ltd. Hitachi, Ltd. Isoleika S. Coop. Jiangsu Sanyou Dior Energy-Saving New Materials Co., Ltd. JIOS Aerogel Pte Ltd. Kingspan Group plc Knauf Gips KG Kurabo Industries Ltd. KyungDong One Co., Ltd. LG Hausys, Ltd. Morgan Advanced Materials plc (Porextherm Dammstoffe GmbH) Nano Tech Co., Ltd. OCI Company Ltd. Panasonic Corporation PBM Insulations Pvt. Ltd. Protective Polymers Ltd. Sealed Air Corporation (Kevothermal, LLC) Sichuan Micolon Vacuum New Material Co., Ltd. Siltherm Group Holdings Limited Svenska Aerogel Holding AB TAASI Corporation Trelleborg AB TURNA d.o.o. Turvac, inovativne izolacije, d.o.o. Vaku-Isotherm GmbH va-Q-tec AG

The vacuum insulated panels (VIP) design comprises a sandwich structure consisting of an outer film, envelope material, and core material. The outer film is made of a high barrier multilayer film. Its function is to...

Aerogel is a unique synthetic material composed of 90% air trapped within a porous, sponge-like nanostructure derived from an alcohol gel precursor. Despite the lightweight composition, aerogels exhibit high structural strength, making them traditionally valued...

Shopping Cart

Scroll to Top

Request Sample

Global Advanced Insulation Materials Market, 2023-2028

Please fill out our form and we will get back to you.